QR Codes and Contactless Payments: A Revolution in Transactions and Word Limits

QR Codes and Contactless Payments: A Revolution in Transactions and Word Limits

Oct 20, 2023 14:30 PM

QR Codes and Contactless Payments: A Revolution in Transactions and Word Limits

Oct 20, 2023 14:30 PM

From paying for pizza with a text message to making use of QR codes to pay while parking in a car or tapping your cellphone to purchase food at the cafe, payments are becoming quick, easy, and seamlessly integrated into customers' journeys.

The ever-changing world of payment processing as well as the introduction of advanced payment technology is leading to significant changes in how companies operate as well as how consumers are interacting with them. With more expectations, customers are looking for secure, user-friendly, and quick contactless payment when they make purchases.

In the wake of 2008's financial meltdown, the market for payments has experienced an explosion of new players, ranging from finance technology to non-financial businesses. This surge of new players has prompted new payment techniques and has blurred the boundaries between payments, banking, and commerce.

These developments are quickly altering the payment landscape, which makes it difficult for those who are not familiar with the subject to understand. This article will provide important information about the current payment options, the key market players, the size of the market, and expected growth, as well as the main forces driving changes in the next few years.

Payment methods cover the different ways that consumers can pay for the products and services they purchase. They can be broadly classified into traditional payment options such as cash, digital, or electronic payment methods like credit and debit cards.

Additionally, payments can be classified based on their compatibility with online or in-store purchases. They are used in both consumer-to-business (B2C) and business-to-business (B2B) situations, as well as for the transfer of money to a bank account. This section will outline the most popular payment methods.

Cash is the term used to describe a physical form of money, like coins and banknotes, that is widely used as a means of exchange for services and goods. It is tangible evidence of the value that is commonly utilized to make transactions, notably in face-to-face transactions.

Cash is regulated and issued by central banks, government agencies, and central banks, which makes it a central kind of currency. Instant liquidity is easily accessible, and it is a popular and easy method of paying across economies and societies around the globe.

Card payments are transactions performed by using a credit or debit card. Instead of cash in physical form, businesses or individuals can make use of a credit account issued by a financial institution to purchase items or pay for services. These transactions are processed electronically using card readers or payment gateways online.

The bank transfer, which is also referred to by the name account-to-account (A2A) payments, is a common method of moving money from one bank account into another. They permit businesses, individuals, and organizations to transfer funds electronically between multiple banks, both in the United States and internationally.

Several advantages exist for bank transfers. They are typically regarded as an extremely secure method of transferring funds, particularly when they are larger, since they offer a paper record that records the transactions. Bank transfers are simple to make online or through mobile banking apps. This makes branch visits unnecessary.

Digital wallets, sometimes referred to as mobile wallets or e-wallets, are platforms made of virtual technology that permit users to save their personal information about payments securely and perform electronic transactions. They offer the convenience and security of making payments on tablets, mobile devices, and desktop computers.

Digital wallets can be used to store different kinds of information about payments, like credit or debit card details and bank account numbers, as well as cryptocurrency. Users can connect their payment options to their wallets digitally and not have to carry physical cash or input details for each transaction.

To make a purchase, customers can access their wallets online to verify their identity by using a fingerprint, password, or face recognition. Select the payment method and sign off on the transaction. The digital wallet is secure in transmitting payment details to the retailer, which ensures the transaction is quick and straightforward.

A mobile wallet can be described as a kind of digital wallet that can be accessed via an application for mobile devices like smartwatches or smartphones. Mobile wallets are extremely popular because of their ease of use, speed, convenience, and adaptability.

Peer-to-peer (P2P) applications enable money transfers between users with separate bank accounts and connect to banks' credit or debit cards. They come in many types, such as separate services as well as bank-centric, mobile OS-centric devices, and social media-based services.

Payments embedded seamlessly connect payment functions directly into third-party platforms or applications, which allows users to conduct fast and easy transactions without having to leave the application. They enhance the customer experience, boost conversion rates, and provide valuable information.

Integration of embedded payments typically requires partnerships between the application provider, payment providers, or financial institutions. This partnership allows the application to secure and process payments, handle transaction information, and guarantee conformity with applicable laws.

Buy Now, Pay Later (BNPL) is an option for financing that allows consumers to make purchases in a series of installments over some time. This technique, also referred to as installment lending, is gaining popularity because of technological advancements that allow for a quick and easy experience both in stores and online.

With BNPL, the purchase is divided into equal installments, which are, on average, four per month without interest. The majority of customers go through a simple online application process that will not impact their credit score except if they fail to make the payments scheduled. There are penalties for late payments and non-payments.

A payment link is a great method of directing customers to a specific checkout page that allows them to make the payment. It is accessible through websites, texts, emails, or posts on social media. Payment links are linked to payment gateways that use encryption and tokenization to protect information about payment transactions.

Businesses can utilize payment links as a straightforward method to solicit and accept online payments without having an online site or checkout page. These links could take the form of QR codes, URLs, or payment buttons created through the sellers.

Payment via text, also referred to as SMS payments or text-to-pay, is a method of making payments on mobile devices via text. Customers can make a payment simply by texting an exact phrase or code-specified phone number.

The typical payment procedure involves the linking of a payment method, such as a credit or debit card or bank account, to the mobile number of the customer. Following authorization, the agreed-upon amount is credited to the payment method linked.

Direct debit (DDD) is an alternative method that permits authorized businesses to withdraw funds directly from a client's bank account. It is often used to pay regular payments, like utility bills and membership fees, as well as loans, charitable donations, and B2B invoices.

Recurring payments function in the same way as direct debits. These payments also need prior authorization from the consumer. However, instead of an account at a bank, the payments are made from a credit or debit card. This method of payment is utilized, for example, for the payment of subscriptions that require quick clearing.

Direct debits and recurring payments serve similar purposes. Both can be used to make regular payments, whether they're fixed or variable in their amount. They provide convenience to the business and the user and guarantee prompt payment without manual intervention.

COD is one of the payment methods whereby the buyer buys an item or service either via card or cash at the moment of delivery. When using COD, the buyer makes an order and chooses to pay upon receipt of the product. The payment is sent directly to the carrier at the address of the buyer.

It is a well-known payment option for people who do not want to make payments online or don't have access to electronic payment options. It is convenient and secure since customers can look over items before making a purchase. But sellers could face dangers like fraudulent or non-payment orders.

Payments using cryptocurrency involve the use of digital currencies, like Bitcoin or Ethereum, to act as a method to exchange goods or services, removing any need to use intermediaries such as banks. The transactions depend on blockchain technology, which guarantees the security and integrity of transactions.

To make a cryptocurrency-based payment, both the payer and the recipient must have digital wallets such as Coinbase with unique cryptographic keys. The sender provides the address of the wallet that will be used by the recipient and the amount that needs to be transferred, while miners in the blockchain network confirm the legitimacy of the transaction.

B2B payments involve the exchange of currencies to purchase goods or services between two companies. They could be one-time or recurring transactions. B2B payments are more complicated than B2C transactions, as B2B processing takes greater time to review and complete the transaction, which could be weeks or days.

Paper Checks:While they are no longer in use in a B2C context, they are the most popular payment method used in B2B transactions. They provide a clear paper trail; however, they do come with disadvantages, like the risk of human errors and bounced checks, an increase in processing complexity, and slow clearing times.

Automated Clearing House (ACH): The ACH system is the equivalent of writing a check. It involves taking money from the buyer's bank account and transferring it into the account of the seller. This is a great method for recurring payments that are scheduled between companies.

Credit Card Payments:Made with credit cards, this is a reliable and long-standing method. However, they typically come with large charges for both parties and are subject to limits on spending, which could be problematic for large-volume business transactions. Additionally, payments made with credit cards are easily tracked on monthly statements.

Wire Transfers:> Wire transfers are a common payment method that involves the direct transfer of funds between banks. They are safe, but they need a few setup and implementation procedures. Wire transfers generally do not have restrictions on currency for transactions.

Digital Payment Platforms:These platforms can be used to transfer funds between accounts. It is efficient in processing funds at lower costs and a quicker rate than traditional methods because of their digital nature. Some examples of platforms include Dwolla, Google Pay, Skrill, PayPal, and Venmo.

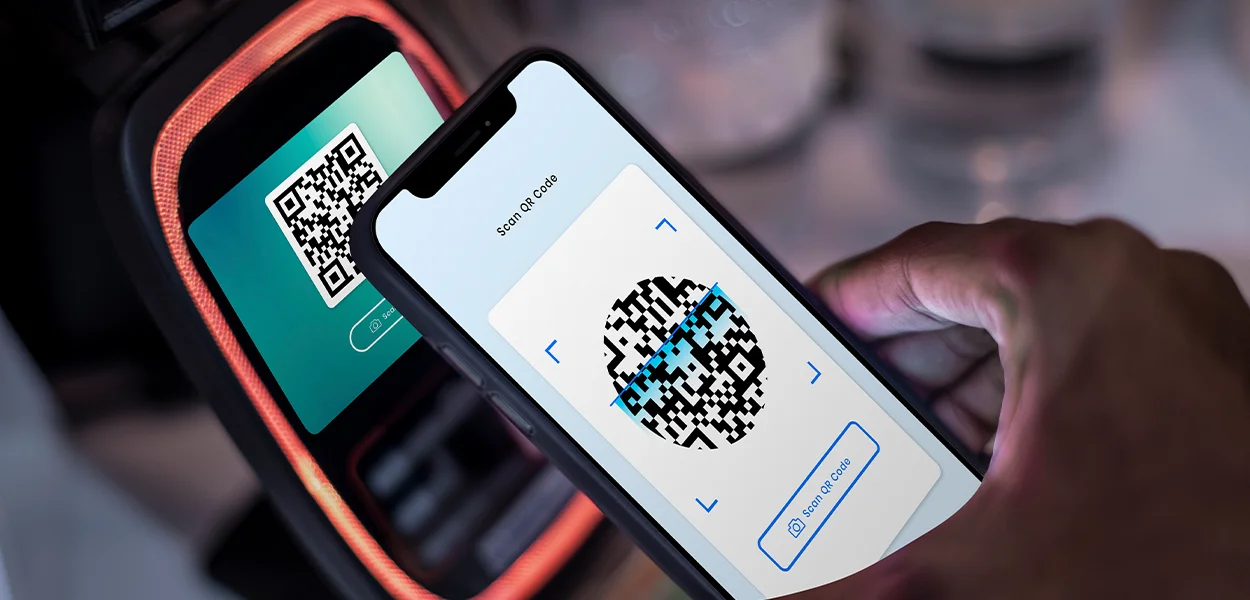

Due to its numerous advantages, QR code technology is being adopted at a rapid pace across the globe.

The way we pay for or interact with the internet has changed with QR codes as well as QR code payment. Two-dimensional QRcodes can store many details within a compact area. They can be used as a device for encoding and retrieving diverse types of information due to their large capacity for data, their ability to correct errors, and their rapid scanning.

The widespread use of QR codes has improved the experience for customers, simplified transactions, and provided new loyalty and marketing possibilities for companies. QR codes can provide businesses with an affordable and secure payment option that is in line with the rising demand for mobile and digital payments. Because they can effectively store and transfer data efficiently, QR codes have emerged as an important asset for companies across a variety of industries.

Strategy

Design

Blockchain Solution

Development

Launching

Testing

Maintenance

Contact US!

Plot 378-379, Udyog Vihar Phase 4 Rd, near nokia building, Electronic City, Phase IV, Sector 19, Gurugram, Haryana 122015

Copyright © 2026 PerfectionGeeks Technologies | All Rights Reserved | Policy

Strategy

Design

Blockchain Solution

Development

Contact US!

Plot 378-379, Udyog Vihar Phase 4 Rd, near nokia building, Electronic City, Phase IV, Sector 19, Gurugram, Haryana 122015

1968 S. Coast Hwy, Laguna Beach, CA 92651, United States

Copyright © 2026 PerfectionGeeks Technologies | All Rights Reserved | Policy